Bull or Bear —We Still Get Paid

5 overlooked dividend stocks set

for 15%+ total returns per yearregardless of what markets do next.

Hi, I’m Brett Owens, Chief Investment Strategist at Contrarian Outlook.

For most income investors, the problem isn’t a lack of opportunity.

It’s the false belief that higher returns require taking bigger risks.

They don’t.

Over the years, I’ve found that some of the most consistent 15%-per-year total returns come from boring, cash-rich dividend stocks that most investors overlook entirely.

I call this approach the Recession-Resistant Retirement Plan.

It’s built for investors who want to grow their income steadily—without chasing the next hot stock, speculating on unproven ideas, or placing bets they’d be uncomfortable explaining at the dinner table.

Because when it comes to funding your retirement, gambling on unicorns isn’t bold.

It’s unnecessary.

This isn’t about predicting recessions or timing market tops.

It’s about owning the kinds of dividend-paying businesses that keep generating cash—and rewarding shareholders—through inflation, slowdowns, bear markets, and everything in between.

- Companies with durable cash flows.

- Management teams that raise payouts consistently.

- And balance sheets strong enough to support both dividends and long-term growth.

When you put those pieces together, something powerful happens:

You don’t just collect income. You position yourself for reliable 15%+ total returns—year after year.

And today I’m going to share my exact process with you. Then I’m going to give you …

The Time-Tested Way to Earn

15% Per Year From Dividend Stocks

— Without Taking Big Risks —

There’s a portion of the market most investors never bother to explore.

It’s filled with companies that look unremarkable at first glance—businesses that rarely make headlines, don’t dominate financial TV, and almost never show up in “hot stock” conversations.

That’s exactly why they’re so often mispriced.

Beneath the surface, these companies share a specific set of characteristics that quietly drive long-term returns:

- Steadily rising dividends

- Disciplined capital allocation

- Stock prices that lag their underlying cash-flow growth

When those factors align, they create a powerful dynamic—one that allows patient investors to earn double-digit total returns with far less volatility than the broader market.

Over time, I’ve distilled this pattern into a simple framework I use to evaluate every income stock I consider.

It consists of three simple pillars.

We’ll get into all of the details in just a moment, but first, let me tell you a little bit more about myself …

Today I’m writing to you from Sacramento, where I live with my family. It’s an interesting time to be here, with the tech sector continuing to pour huge amounts of money into AI, and the technology starting to root itself in the broader economy.

You may have seen me on CNBC, Yahoo Finance or NASDAQ, where I’ve been called on to share my methodology for collecting consistent, predictable and reliable retirement income without making any wild, speculative bets that keep you up at night.

You see, I take a strategically contrarian approach to the markets.

And for the past several years, I’ve helped thousands of readers fund their retirement thanks to what I call “Hidden Yield stocks.”

For example:

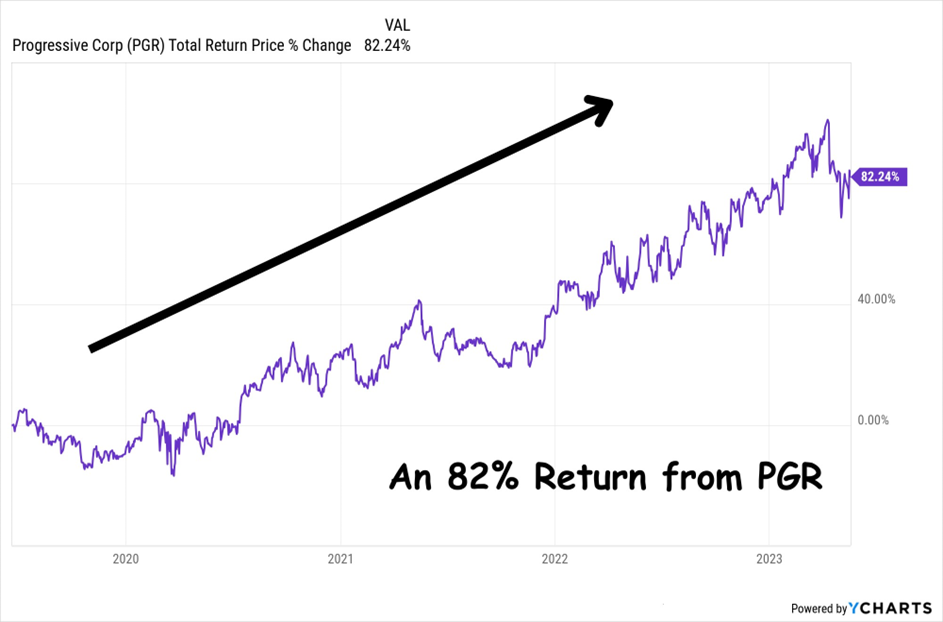

82% on Progressive Corp. in Just Under 3 years

22% on Microsoft in just 3 months

83% on Synnex Corp. in 24 Months

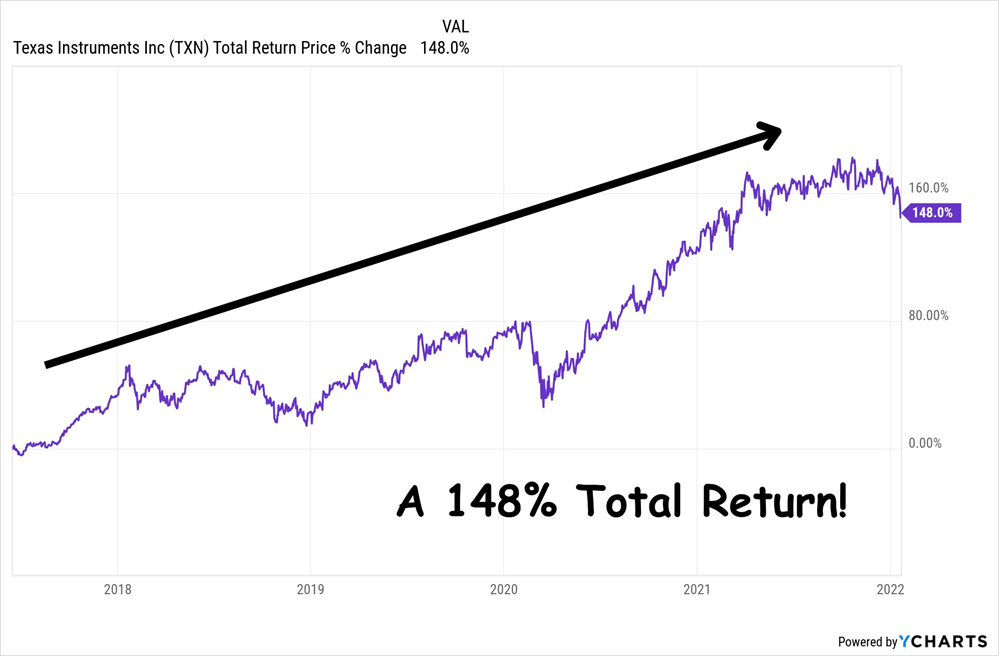

148% on Texas Instruments in just over 4 years

Now, I know these aren’t the huge 500% … 1,000% … or 5,000% overnight gains you hear other gurus CLAIMING they can get you.

But—as you’ll see in just a moment—outrageous claims like these are nothing more than overhyped promises designed to separate YOU from your money.

And to be clear, not all recommendations play out as well as the four examples above. Investing in the stock market is inherently risky, and some recommendations have lost money.

So we level-headed contrarians don’t chase unicorns.

We don’t listen to smiling swindlers.

We don’t put our family’s futures in jeopardy.

Instead, my readers and I focus on …

Doubling Our Money Every 5 Years with

15% Total Returns Per Year on Little-Known

“Hidden Yield Stocks”

However, this is just one small part of what I do.

My real aim is to help investors safeguard their retirement from recessions with low-volatility—but highly lucrative—investments that consistently pay you, whatever direction the market goes.

This method lies very close to my heart and ethics.

You see, my first experience in the markets was brutal …

It was 2003, and I’d recently graduated from Cornell University and was designing computer systems for Fortune 500 companies. For the first time in my life, I was making money. So I decided to hire a broker to help grow my savings.

This guy had countless credentials and certifications, years of experience, and he talked a great game.

Without hesitation, I hired him.

The result?

Just one year later, this so-called expert had literally lost nearly ALL my money. Everything. Years of saving and investing, gone.

As you can imagine, I was furious. However, thanks to this experience, I came to a huge breakthrough. I realized that nobody is EVER going to care about MY money, MY future, MY retirement and MY family as much as I do.

And, I realized, if I wanted to retire rich, I needed to take control of my money.

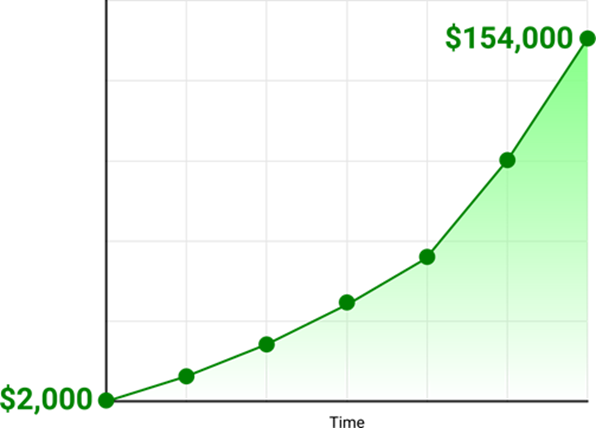

Anyway, with this realization, I decided to learn everything I could about investing. I was absolutely relentless. And after a few bumps in the road, it paid off, starting with a measly $2,000 that I turned into $154,000 in just 48 months!

Obviously, this sort of performance doesn’t go unnoticed …

Shortly afterward, I was invited to join a famous financial publication as an editor.

At first it was great. We helped our readers take home huge profits, exponentially grow their portfolios and finally create the financial freedom they’d been chasing their whole life.

However, as time passed, things started to change …

Instead of focusing on secure, safe stocks with huge upside, they started recommending all sorts of highly speculative, high-risk “investments” like obscure cryptocurrencies, volatile penny stocks and many other questionable opportunities.

Anyway, this didn’t sit well with me.

I believe financial analysts like me have an ethical and moral duty to help our readers safely grow their money—not recklessly gamble it away on some pie-in-the-sky idea.

Which is why I decided to set up my own research firm—Contrarian Outlook.

Since inception, the goal of Contrarian Outlook has been simple:

All without making any highly speculative bets you can’t tell your spouse about … without trying to time the markets … without the can’t-sleep-at-night worries … and without putting your retirement at risk!

Today I want to share five of my recession-resistant “Hidden Yield Stocks” with you.

My research indicates each of these investments could deliver 15% total returns per year – even as we stumble towards a recession.

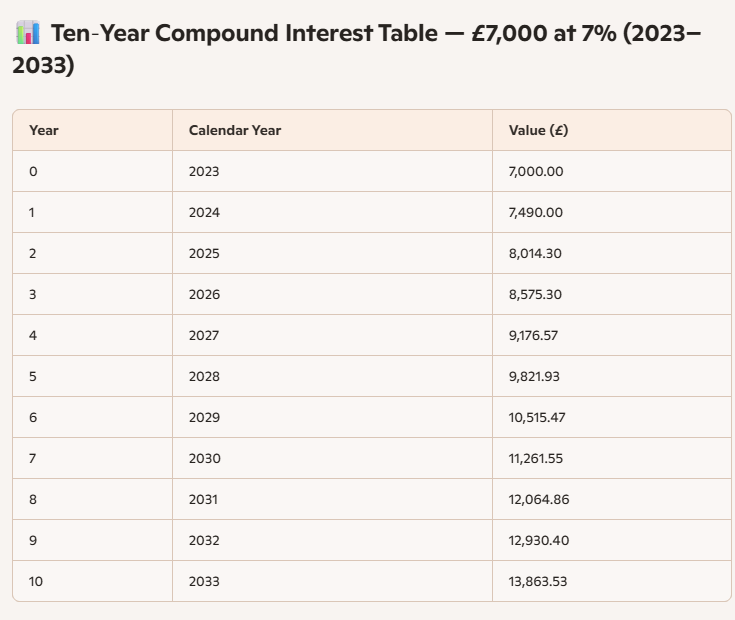

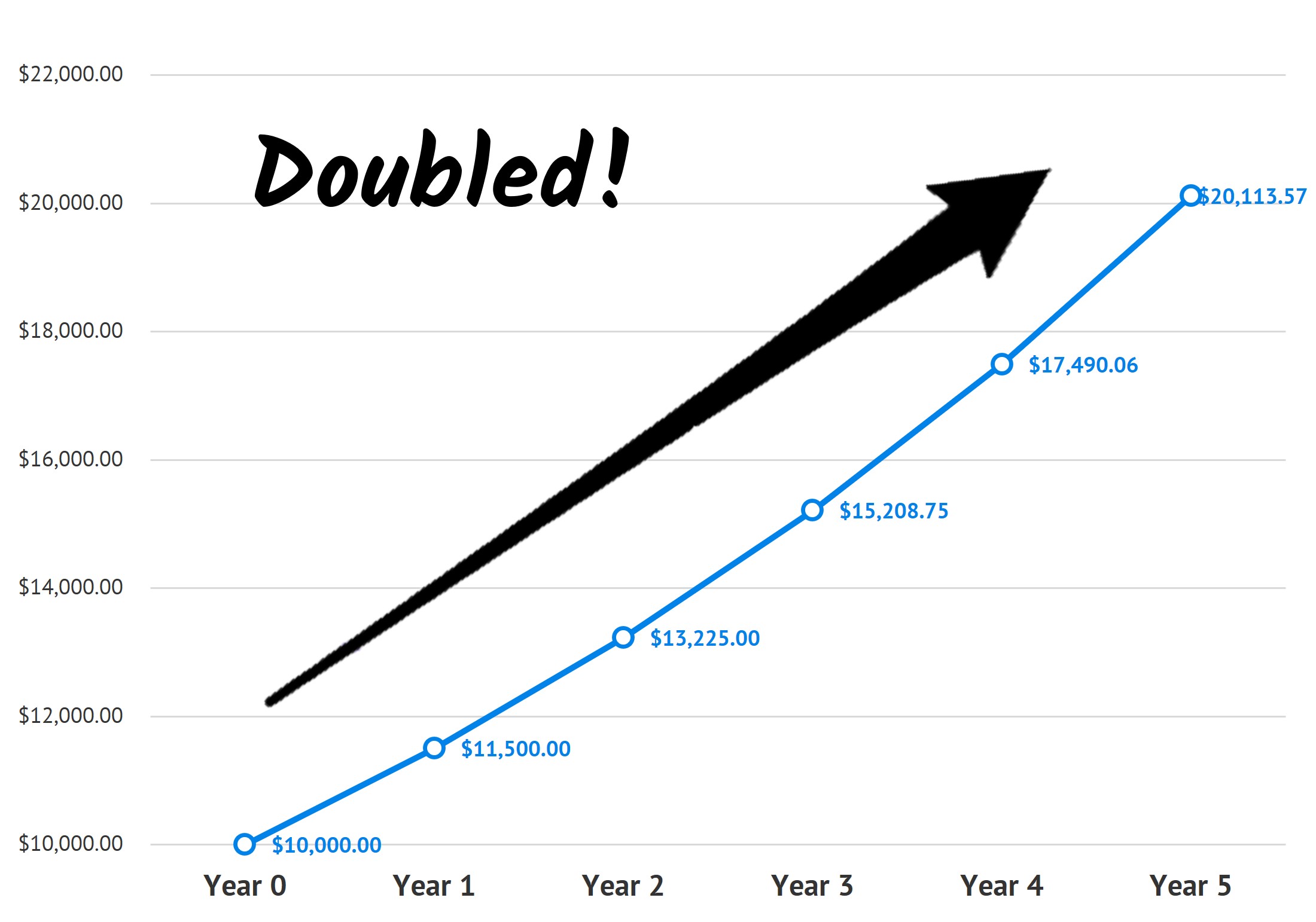

As you can see in the chart below, that’s enough to double your money every 5 years!

15% Average Annual Return on $10,000 Compounded Over 5 Years

Still skeptical?

Good. I would be, too.

Which is why I don’t expect you to just take my word for this.

Instead, I’m going to prove everything to you.

I’ll walk you through my investment approach. I’ll show you how to identify these “Hidden Yield Stocks.” And I’ll give you the cold-hard evidence that proves you can double—even triple—your portfolio without taking on any unnecessary high-risk bets.

Then I’ll give you 5 of my favorite recession-resistant “Hidden Yield Stocks” to buy now.

Here’s the Time-Tested Way to Make

15% Per Year From Stocks

There’s an untapped portion of the market few people know about …

It’s filled with stocks that seem “boring” to the uninformed investor…

Companies that rarely get coverage from the mainstream media …

Contrarian investments that are hiding their true potential …

However, if you look below the surface and read between the lines, these “Hidden Yield Stocks” offer intelligent investors the opportunity to deliver 15% total returns per year—no matter what the wider market does.

How?

Well, the answer lies in what I call “The Three Pillars.”

Pillar #1 – Consistent Dividend Hikes

Pillar #2 – Lagging Stock Price

Pillar #3 – Stock Buybacks

Together, these three pillars allow us to identify the stocks that are undervalued … overlooked … recession-resistant … and primed for major growth.

And by investing exclusively in these “Hidden Yield Stocks,” we can enjoy massive upside with very little downside … plus collect regular, reliable income through healthy dividend payouts!

As I said, today, I want to give you 5 of my favorite “Hidden Yield Stocks.”

But first, let me briefly explain each of the Three Pillars and show you how it helps to predict—with pinpoint accuracy—the direction a stock is going to take.

Pillar #1 – Consistent Dividend Hikes

Most investors approach dividend paying stocks backward.

Here’s how it usually works …

An investor will scan the markets looking for stocks paying a high dividend. After all, if a company is currently paying a high yield, it’s a great investment, right?

Dead wrong!

In fact, looking at the CURRENT yield is one of the slowest ways to grow your money.

You see, if you’re focused on current yields, you’re too late to the party. All the major gains have already been made. You’ll need to settle for earning a paltry 4%, 5%, maybe 6% per year … with minimal stock-price appreciation, too.

Sure, chasing high current yields will provide you with instant gratification, but it won’t give you the recession-resistant income … or the 15% year on year returns we want.

Instead, you need to focus on consistent dividend hikes.

In my opinion, selecting companies with a proven track of increasing their dividend payments is one of the safest, most reliable ways to get rich in the stock market. You see, every time a company raises its dividend, you start earning more from your original investment.

For example:

On a $1,000 initial investment, $30 in dividends equals a 3% return. Later, if the dividends go up to $40 a year, you are effectively earning 4% on your initial $1,000 investment.

As this trend continues, you could easily be earning 10%, 15%, even 20% per year just from rising dividends, as your initial investment never changes.

However, this ever-growing income from dividend hikes is just ONE part of the puzzle. To engineer real growth and quickly double an initial investment, we must combine Pillar #1 with the next two pillars of “Hidden Yield Stocks.”

Pillar #2 – Lagging Stock Price

After years of active investing, I’ve only ever found one surefire way to predict whether a stock will go up or down.

I call it the “Dividend Magnet,” and here’s how it works …

After you’ve identified stocks that are built on the foundations of Pillar #1 (consistently hiking their dividends), you want to narrow your search to companies whose share price LAGS behind the rate of dividend increase.

Why? Well, it’s simple really …

Share prices almost always increase as dividends increase.

This is because as a company hikes its dividend, mainstream investors tend to flock to the stock, chasing the new, higher yields. And this inevitably bids up the share price.

Let me give you a few examples where the dividend acts like a floor to keep bumping the share price higher:

Hershey: Dividend Up 135% Share Price Gains 122%

Mastercard: Dividend Up 691%, Share Price Gains 659%

AbbVie: Dividend Up 312%, Share Price Gains 364%

As you can see in these examples, the stock price lags behind the dividend increases at some point in time …

However, as more investors notice the company’s soaring dividend and buy in, the price lag closes—sending the share price soaring.

So, by investing in the right companies whose share prices have fallen behind despite consistent dividend hikes, you can buy the stock, safe in the knowledge the Dividend Magnet will eventually pull the price up.

Now, investing with Pillar No. 1 and No. 2 alone would stand you in great stead.

However, there’s one final Pillar of a “Hidden Yield Stock” that can rapidly accelerate both the share price and dividend payouts …

Pillar #3 – Stock Buybacks

Uncovering companies that are buying back their stocks is one of the fastest ways to accelerate your gains.

You see, when a company buys back its stock, it is improving every single “per share” metric investors watch (earnings, free cash flow, book value, etc.).

After all, if a company reduces the number of its shares by 50%, its earnings per share will automatically DOUBLE without any actual increase in profits. And I probably don’t need to tell you what will happen next …

Investors quickly bid up the stock’s price to bring it back in line with the value it was trading at before. Indeed, my research shows that simply investing in stocks that are reducing their share counts can help you beat the broader market’s performance.

And it’s important to bear in mind that S&P 500 companies are sitting on huge piles of CASH (more than $1 trillion in all!). They’re rolling out fresh buybacks amid continued economic growth post-pandemic, and they’re getting a nice upside kick in return.

You can see this just by looking at the shares of Union Pacific (UNP), which took an impressive 31% of its stock off the market in 10 years, helping drive a 100% gain in the share price!

And that’s just one example. By targeting cash-rich companies that either continue to buy back shares now or have a long record of doing so (even if they’re holding off today), you can set yourself up for HUGE price gains.

In short …

Combine the Three Pillars … Buybacks,

Dividend Hikes and Price Lags, and Your

Yearly Returns Can Be Absolutely Astounding

My favorite example of dividends and buybacks working in tandem to yank up share prices came in the form of our Mondelez International (MDLZ).

I recommended Mondelez in April 2020, as the world was shutting down. The stock looked cheap … was consistently growing its dividend payments … and management was aggressively buying back shares.

These three pillars told me the stock would skyrocket. And just take a look at what happened …

Over the next three years, Mondelez reduced its share count by 4.6% (orange line in the chart above) while raising its dividend a whopping 35% (blue line).

The market quickly responded, and the stock delivered a 39% price gain (purple line) by the time I recommended selling.

Put it all together and that’s a 48% total return (green line) in just 3 years from a relatively boring (at the time!) company.

Of course not all of my recommendations work out exactly like this one … some better, some worse… and I’m no longer recommending MDLZ today.

But this example shows you that you don’t always need to take big risks or invest in things you don’t understand. All you need to do is sniff out these “Hidden Yield” stocks before the mainstream crowd catches on.

With These 3 Pillars, Uncovering Safe,

Secure Stocks Set to Return 15% Per Year

Is Like Shooting Fish in a Barrel

However, it still takes a lot of work …

You see, although these three pillars can help you beat the market, double your portfolio and enjoy true security in your retirement, you also need to analyze these “Hidden Yield Stocks” in excruciating detail before investing.